Finland, much like the other Nordic countries, has some of the highest income tax rates in the world. The taxation is progressive, the more you earn higher the tax rate, and helps fund social services (education, healthcare, etc.) and welfare programs (pension, unemployment allowance, etc.) among other things (infrastructure, salaries of politicians?).

Anyway, have you ever wondered how taxes actually look like in real life on real paychecks? I’ll provide a detailed breakdown here on my own salary slips.

To make this a bit more interesting, I will demonstrate how taxes are levied in two scenarios, one where I made about 50K USD annually in 2020 and another where I made over 100K USD a year in 2025.

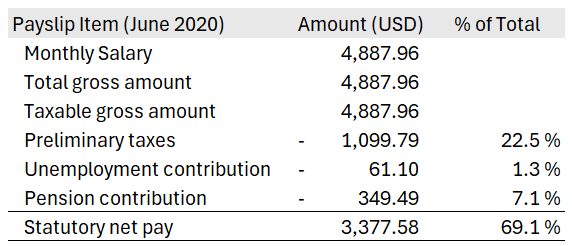

Let’s look at the numbers in the first case. Note that I have converted euro amounts to US dollars with the same FX rate for both the scenarios outlined below.

Statutory net pay is the amount I received in my bank, so I got about 69% of my stated salary in my account whereas 31% of my salary went to the state in various forms of taxes. While it can be argued that I may see the pension contribution paid back to me by the state some day in the future, it is safe to assume it is lost money for now.

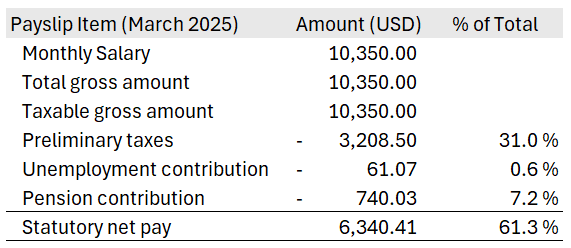

Now the second scenario with over 100K per year salary in 2025. Here, I got only 61% of my stated salary transferred to my bank account whereas 39% went away in taxes. That is a massive contribution towards keeping the country running.

It’s interesting to note that the pension contribution as percentage of the salary did not change meaningfully in the two scenarios, whereas unemployment contribution remained approximately the same in terms of dollar amount.

So there you have it – real Nordic taxes on real paychecks. In case you are curious, all payroll taxes in Finland are automatically deducted by the employer based on a pre-defined, self-declared level of annual income at the start of the year to the tax office, which then issues a tax card outlining the tax rates.