Today (17 March 2026), S&P500 index continued its bounce from the Friday’s low close. SPY is still down by 1.8% year to date (YTD) as of writing this. The market has been mostly range bound with some recent lows on the back of geopolitical conflict in the middle east, with an immediate affect on energy prices & global shipping.

The Volatility Index (VIX) hit an intraday high of 35 on March 9 before reversing, without any significant second spike so far, and closing around the 22 mark today.

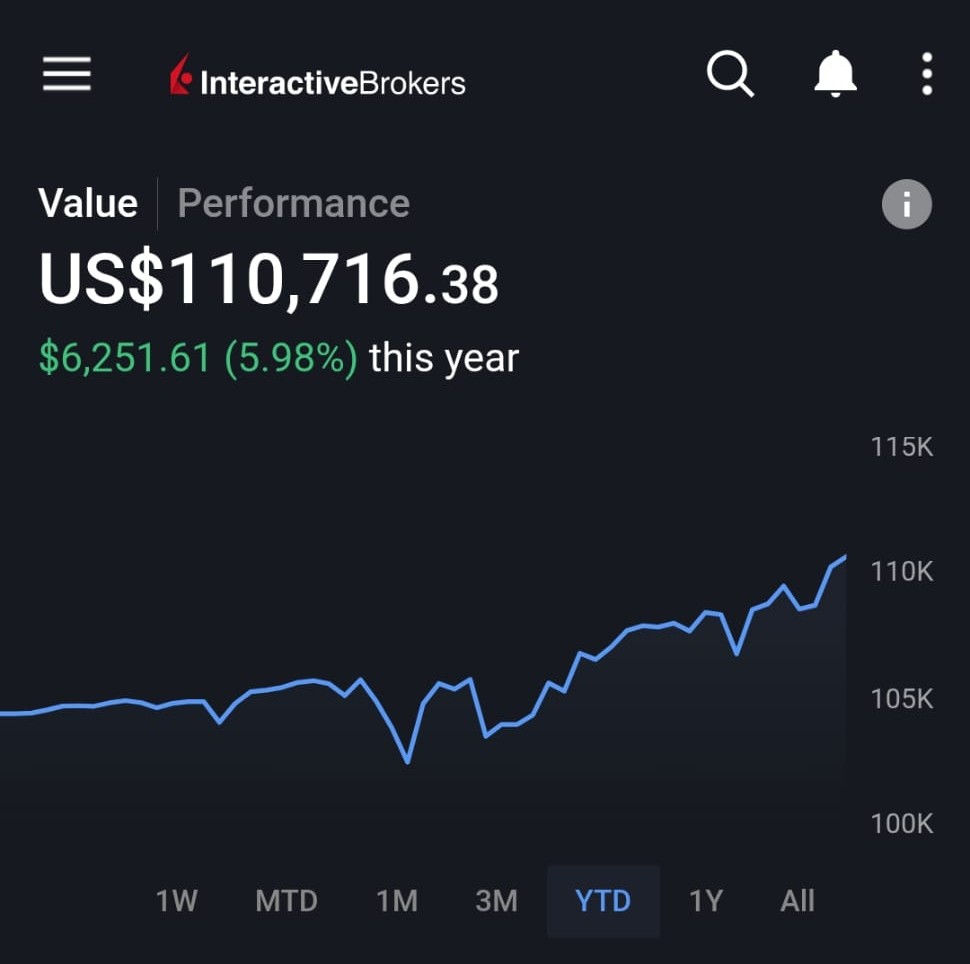

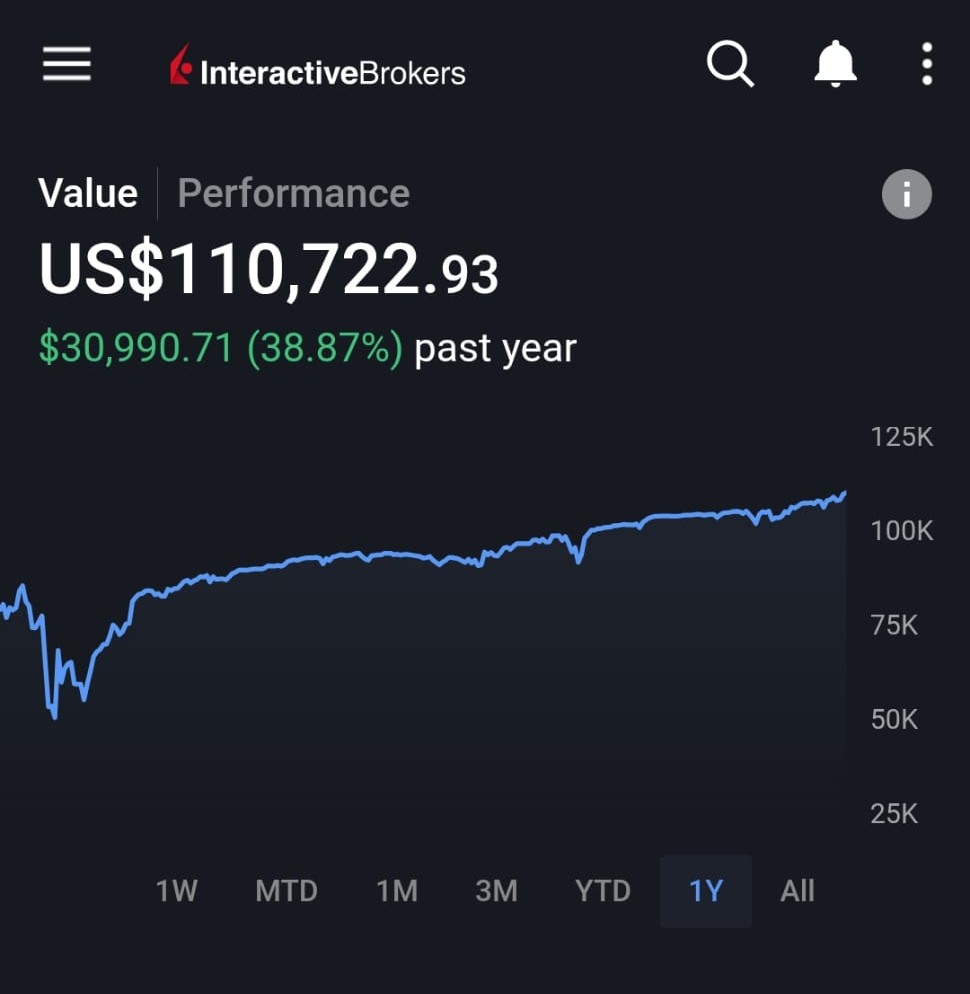

Given this market context, the portfolio I manage has been ticking higher with close to +6% gains YTD and about +39% gains in the last one year compared to +25% gains in QQQ and +18% in SPY.

Some potential reasons for the out-performance of the portfolio could be attributed to:

- Range bound market is conducive to writing/short-selling option contracts.

- High Implied Volatility means higher option premiums to harvest, particularly shorting puts.

- Smaller position size with higher delta for strike selection, mostly just 50% portfolio commitment, at max 70%.

- Trading weekly option expiration, provides highest IV.

- Diversifying trades across time-frames with tactical profit taking.

- And perhaps the most important component – luck.

Once the markets rally with a continued upward trend, the same strategy will underperform the market, hence it is important to adjust the trading strategy according to the market mood.