After a strong rally in S&P500 from April to end of May 2026, June has seen some large moves in both directions, particularly gap ups and gap downs. Moreover, intraday trading range and reversals have been fairly large as well, e.g. 9 June 2026.

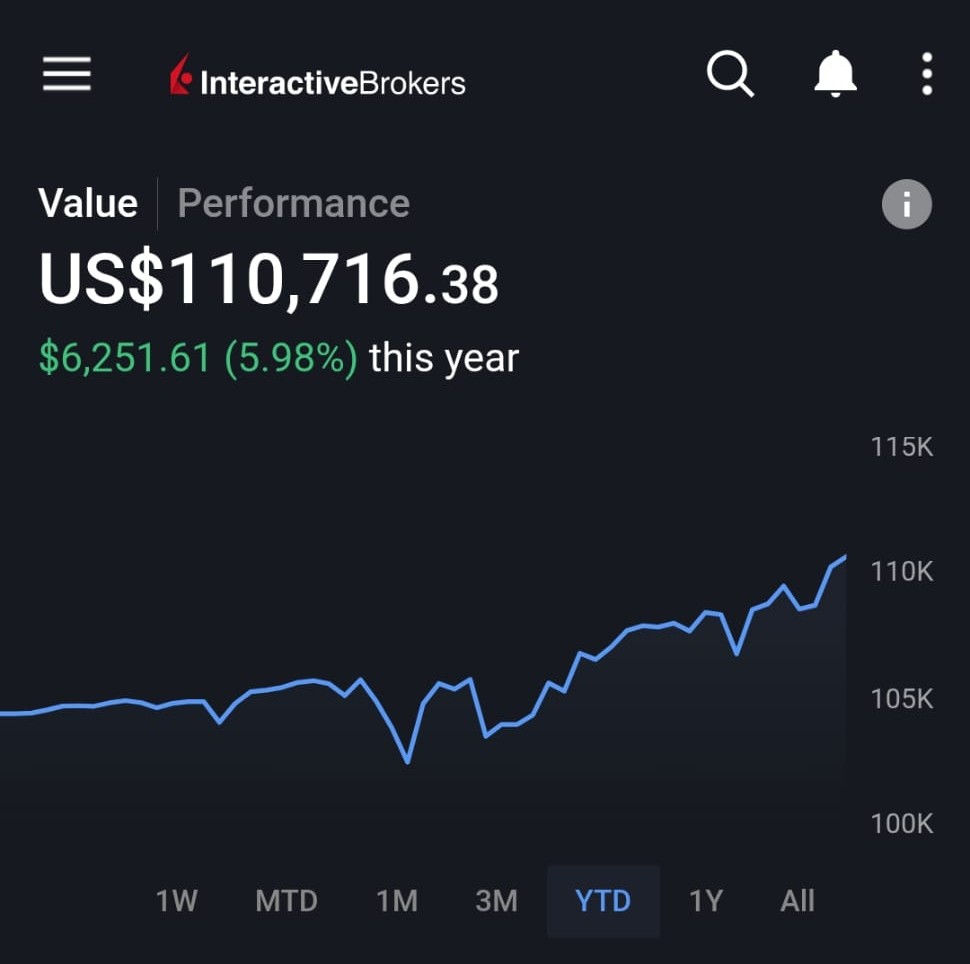

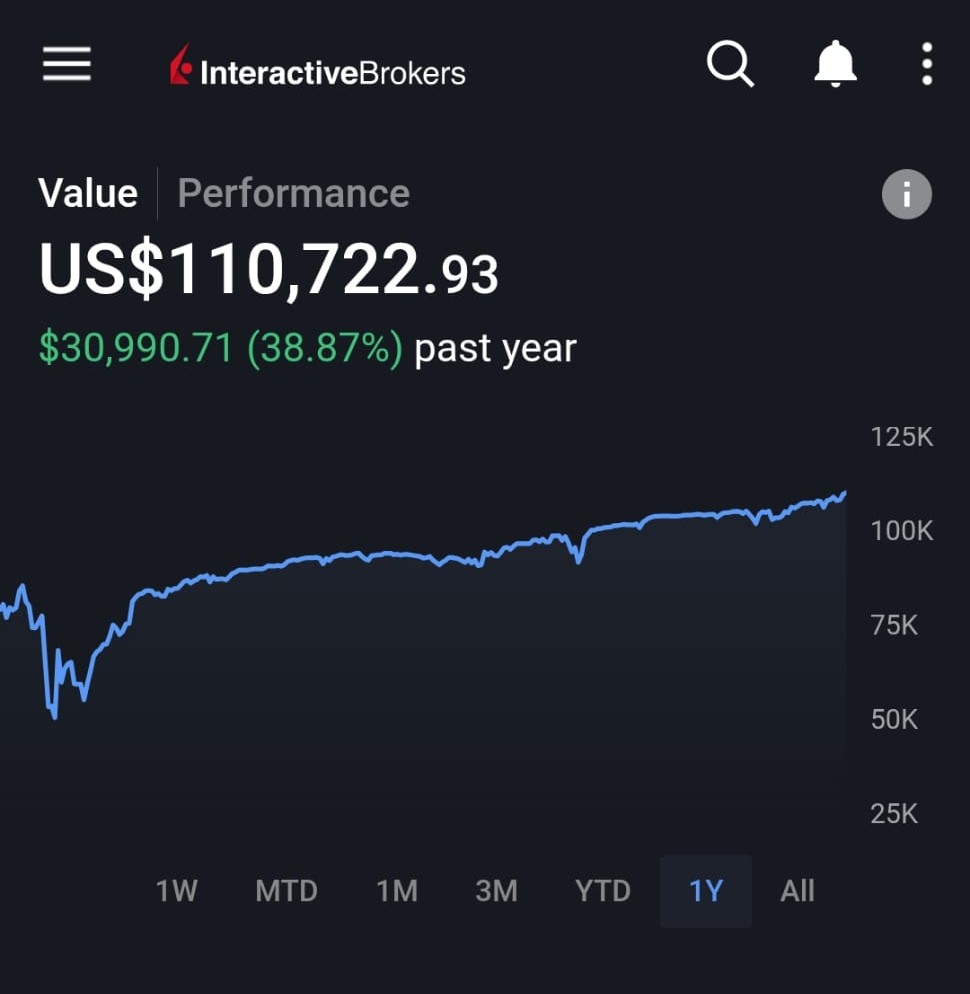

The equity curve of the portfolio I manage has made new highs after a fairly flat period. I’m such a bad trader when markets rally strongly whereas periods of market pullbacks & high volatility generally tend to be more fruitful for me. I really have to get better at riding the market when it does those persistent grind to higher highs.

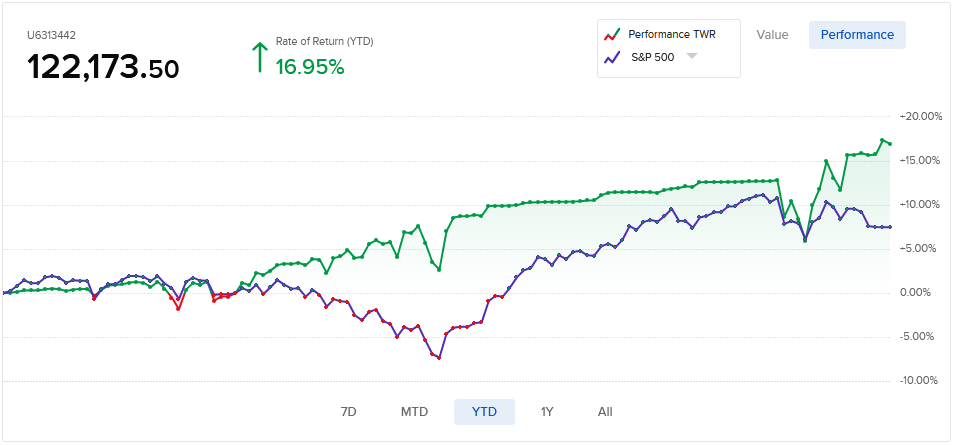

Anyway, just when the market had caught up to my portfolio gains at the end of May, both went down together (I was in a bit too early as usual), however the choppy market provided some good trading opportunities with a high volatility environment and higher premiums to harvest – which helped propel the portfolio to new highs at +17% YTD gains vs the market which is now at about +7% (26 June 2026). With prudent position sizing, delta selection and near term expiration (1-2 weeks), together with tactical profit taking, I managed not only to avoid recent downdowns but to milk out some gains as well.

Vix saw some large % moves, from being around the low 16 mark to crossing over 20 in 2 bars of 4hrs! Note the several clusters of spikes in the 2nd spell at around the 20 mark again.

SPY had some sizable gap ups & gaps downs, and now coiling downwards in a diagonal channel/funnel. Does it breakdown to further lows from here? Would be great if it does so! That would set up for a good move higher in July before reversing again in August perhaps, we’ll see.

SPY on the daily – again would be great if the market comes down to the previous highs at around the 700 price level – revert to its mean values of 200day SMA. That should set it up for the next leg higher.